No products in the cart.

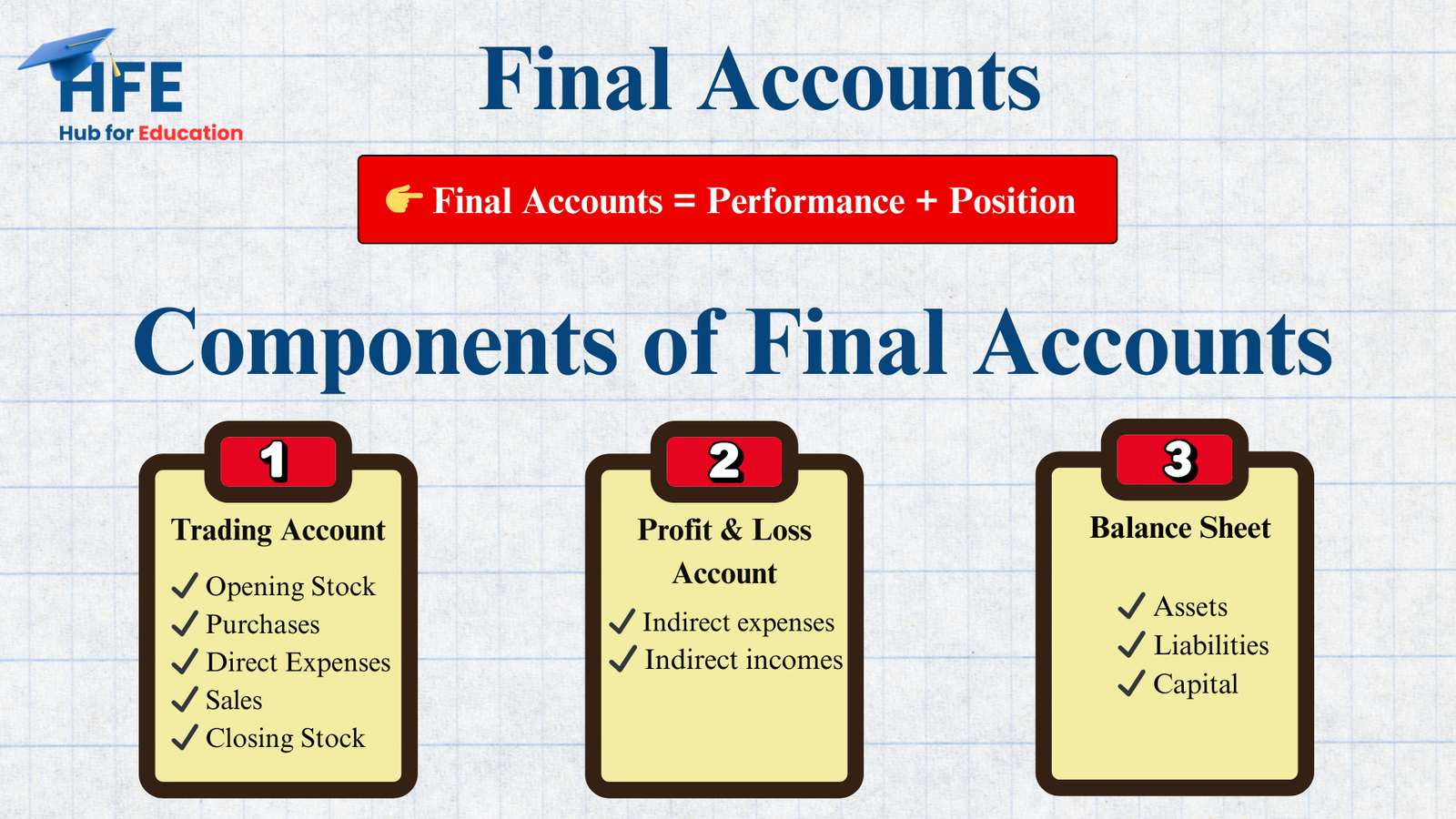

Final Accounts are financial statements prepared at the end of the financial year to determine the performance and financial position of a business.

They help businesses understand:

The Trading Account is prepared to determine the gross profit or gross loss of a business during a particular accounting period.

Items included in Trading Account

The Profit and Loss Account is prepared after the trading account to determine the net profit or net loss of the business.

Items included in Profit and Loss Account

Indirect Expenses:

Indirect Incomes:

The Balance Sheet shows the financial position of the business at a particular date.

It includes three main elements:

Assets are the resources owned by the business. Examples:

Liabilities are the obligations or debts of the business. Examples:

Capital represents the owner’s investment in the business.

Tags:

Share:

Your email address will not be published. Required fields are marked *

Remember Me